Fast-growing number of unreliable payers

The unreliable payer concept has been in the VAT Act since 2013. According to the GFD, in combination with the taxable supply recipient’s liability for unpaid VAT, this concept should serve as an effective tool to fight VAT evasion, whereas the number of unreliable payers has been growing significantly every day.

The VAT Act imposes a duty on the supply recipient to be liable for VAT unpaid by a supplier if the fact that the supplier is an unreliable payer had been made public at the date of supply or, under the July amendment to the VAT Act, at the date of providing consideration. The decisive date is the moment this information was made public. Supply recipients are also liable for VAT unpaid by suppliers if they make payments to unregistered bank accounts.

The GFD’s original Information on the Application of the Unreliable Payer Concept (“the Information”) slightly changed following the July amendment to the VAT Act. The Information summarises circumstances under which VAT payers become unreliable. Generally, these involve cases in which public interest in the proper collection of VAT has been jeopardised.

To be more concrete, these involve for instance situations where the VAT payer reports a cumulative VAT undercharge for at least three calendar months. The amount of the permitted undercharge is now CZK 500 thousand, compared to CZK 10 million as per the original Information.

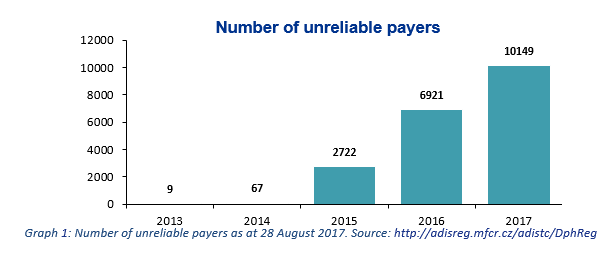

You can generate a list of all unreliable payers (and persons) directly at the Tax Portal (adisreg.mfcr.cz). More than 10 000 unreliable payers were reported at the end of August 2017, accounting for about 2% of all VAT payers in the Czech Republic.

It is therefore quite vital to set appropriate control mechanisms, review the reliability of suppliers and make payments only to registered bank accounts.